Major Update: Key Changes to Proposed Division 296 Superannuation Tax

The proposed Division 296 tax, targeting high-balance superannuation accounts, has been significantly updated. In October 2025, the government announced several critical amendments intended to create a fairer and more practical system for high-wealth individuals.

The proposed Division 296 tax, targeting high-balance superannuation accounts, has been significantly updated. In October 2025, the government announced several critical amendments intended to create a fairer and more practical system for high-wealth individuals.

These changes, which delay the start date and introduce a tiered structure based only on realised earnings, have major implications for affected individuals and demand immediate review of existing superannuation strategies.

What is the Division 296 Tax?

Division 296 proposes an additional tax on the earnings of superannuation balances that exceed a specific threshold. It is designed to ensure a higher level of tax is paid on the concessional environment benefits enjoyed by the wealthiest superannuation members.

The Four Key Updates You Need to Know

The amendments announced in October 2025 reshape the implementation of this tax:

1. Delayed Start Date and First Assessment

New Start Date: The proposed implementation has been delayed by one year to 1 July 2026.

First Assessment: The first Division 296 tax assessments will relate to the earnings accrued during the 2026–27 financial year and will be issued in the 2027–28 financial year.

2. The Move to Realised Earnings Only

In a crucial shift that addresses widespread industry concerns regarding liquidity and complex valuations, the tax will now only apply to realised earnings.

What is Included: Only earnings that have been crystallised into cash or assets upon sale will be considered. This includes:

Interest and Dividends

Rental Income

Capital Gains from sold assets

What is Excluded: This change effectively removes the complex issue of applying the tax to unrealised earnings (paper gains), which previously posed significant administrative and liquidity challenges, particularly for investments in private businesses or property.

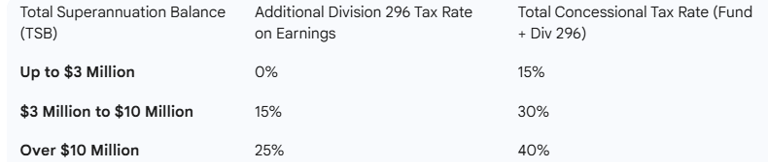

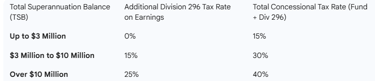

3. New Progressive Tiered Tax Rates

The single, flat 15% rate has been replaced with a progressive, two-tier system, applying in addition to the standard 15% tax rate already paid by the super fund:

Tier 1: An additional 15% tax on earnings for balances between $3 million and $10 million.

Tier 2: An additional 25% tax on earnings for balances over $10 million

4. Indexed Thresholds to Combat 'Bracket Creep'

Both the $3 million and $10 million thresholds will be indexed annually according to the Consumer Price Index (CPI). This is a vital measure to ensure that the thresholds maintain their real value over time, preventing individuals from being drawn into the Division 296 tax net solely due to inflation (bracket creep).

Who Needs to Take Action?

Division 296 will apply to individuals whose Total Superannuation Balance (TSB) across all superannuation accounts exceeds $3 million at the end of the financial year.

It is critical to note:

Individual Assessment: This is an individual tax assessment, separate from the super fund’s own tax calculation.

Payment Options: Affected members will have the option to pay the tax personally or to have the required amount released from their superannuation fund.

Planning Considerations Before 1 July 2026

While this legislation has not yet passed into law and remains subject to further consultation, individuals who anticipate being impacted should use the delayed implementation date to review their financial strategies.

Review Asset Timing: Consider the timing of asset sales to manage when capital gains are realised, especially before the 1 July 2026 start date.

Assess TSB: Understand how your current Total Superannuation Balance tracks against the indexed $3 million and $10 million thresholds.

Seek Advice: This is a complex area. We strongly recommend speaking with a qualified financial advisor or tax professional to model the impact of Division 296 on your retirement savings strategy.

Disclaimer: The information provided in this article is based on proposed legislation and announcements and is subject to change until the bill passes into law. It does not constitute personal financial or tax advice.