The Multi-Generational SMSF: Understanding the Concept of Segregation

In a "normal" SMSF, everything is pooled, members share the bank accounts and investments proportionally. With segregation, specific assets are legally and administratively tied to specific members.

While many Australians manage their superannuation independently, some families—particularly within cultures that prioritize collective wealth—look to the "Family SMSF" as a vehicle for intergenerational prosperity. Current Australian regulations allow for up to six members within a single SMSF, creating opportunities for families to manage assets under one structure.

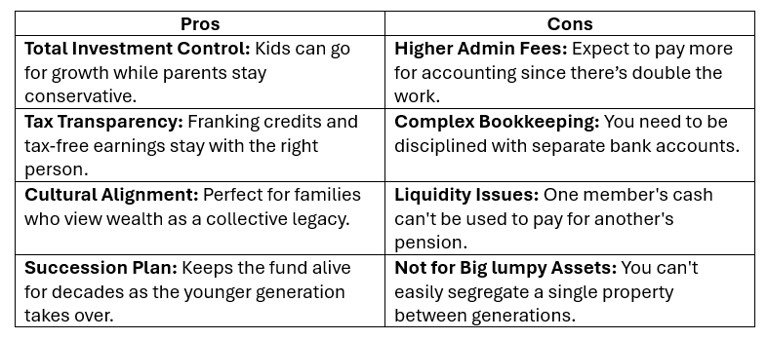

However, a common challenge in a multi-generational fund is the divergence of goals. A member aged 65 typically has different investment objectives (income and stability) compared to a member aged 35 (long-term growth).

The fix? Segregated Accounts.

What’s the deal with Segregation?

To address these differing needs, some funds utilize a structure known as Segregated Accounts.

The "Apartment Building" Analogy One way to visualize this is as an apartment building. All members share the same "front door" (the SMSF legal structure), but each member or couple has their own "private unit" (their own distinct bank accounts and investment assets).

In a traditional "pooled" SMSF, all assets are combined, and members share in the fund's total investment performance proportionally. In a segregated structure, specific assets are legally and administratively tied to specific members.

Functional Considerations

From a factual perspective, segregation changes how the fund operates in two primary areas:

1. Tax and Earnings Treatment By keeping accounts separate, the tax treatment of the fund becomes more distinct:

Tax Segregation: Assets tied to members in the "Pension Phase" can earn income that is exempt from tax (Exempt Current Pension Income), while assets tied to members in the "Accumulation Phase" remain subject to the standard 15% tax rate.

Attribution of Credits: Franking credits and investment returns are attributed directly to the account that holds the asset, rather than being shared across the entire fund's member base.

2. Administrative Realities It is a common misconception that a multi-generational SMSF significantly reduces accounting costs. From an administrative standpoint, segregation requires significantly more tracking. Because every bank statement, dividend, and trade must be attributed to a specific "bucket," the accounting work is essentially doubled compared to a pooled fund. Consequently, the professional fees for a segregated fund are typically higher than those for a standard single-member or couple fund.

How it works in the real world (The Expense Hack)

In practice, families using this structure often aim for a "fairness" model regarding fund expenses (such as audit and accounting fees). A common factual method for handling these is as follows:

Central Payment: One "main" account (often the parents’) pays the total fund invoice to the service provider.

Internal Transfer: The other members (the children) then transfer their portion of the fee (e.g., 50%) into the parents' account to reimburse the fund.

This method is used to keep bookkeeping clear and ensure that one member’s balance is not unfairly burdened by the administrative costs of the entire family group.

At a Glance: Is Segregation Right for Your Family?

A multi-generational SMSF with segregated accounts is a complex structure that allows for individualized investment strategies within a single legal entity. While it offers clarity regarding tax and asset ownership, it also carries higher administrative requirements and trustee responsibilities.

Beyond generational planning, segregation is an essential strategy for blended families. For couples with children from previous marriages, keeping investment 'buckets' separate is a powerful way to mitigate potential disputes and ensure estate intentions are honoured. While segregation is a sophisticated tool for connecting family members under one roof, its success relies on meticulous planning and clear boundaries.

The information provided in this article is general in nature and does not constitute personal financial, legal, or tax advice. It has been prepared without taking into account your personal objectives, financial situation, or needs. Before acting on any information, you should consider the appropriateness of the information having regard to your objectives, financial situation, and needs. We recommend seeking professional advice from a qualified financial advisor, accountant, or legal practitioner before making any decisions regarding your SMSF.